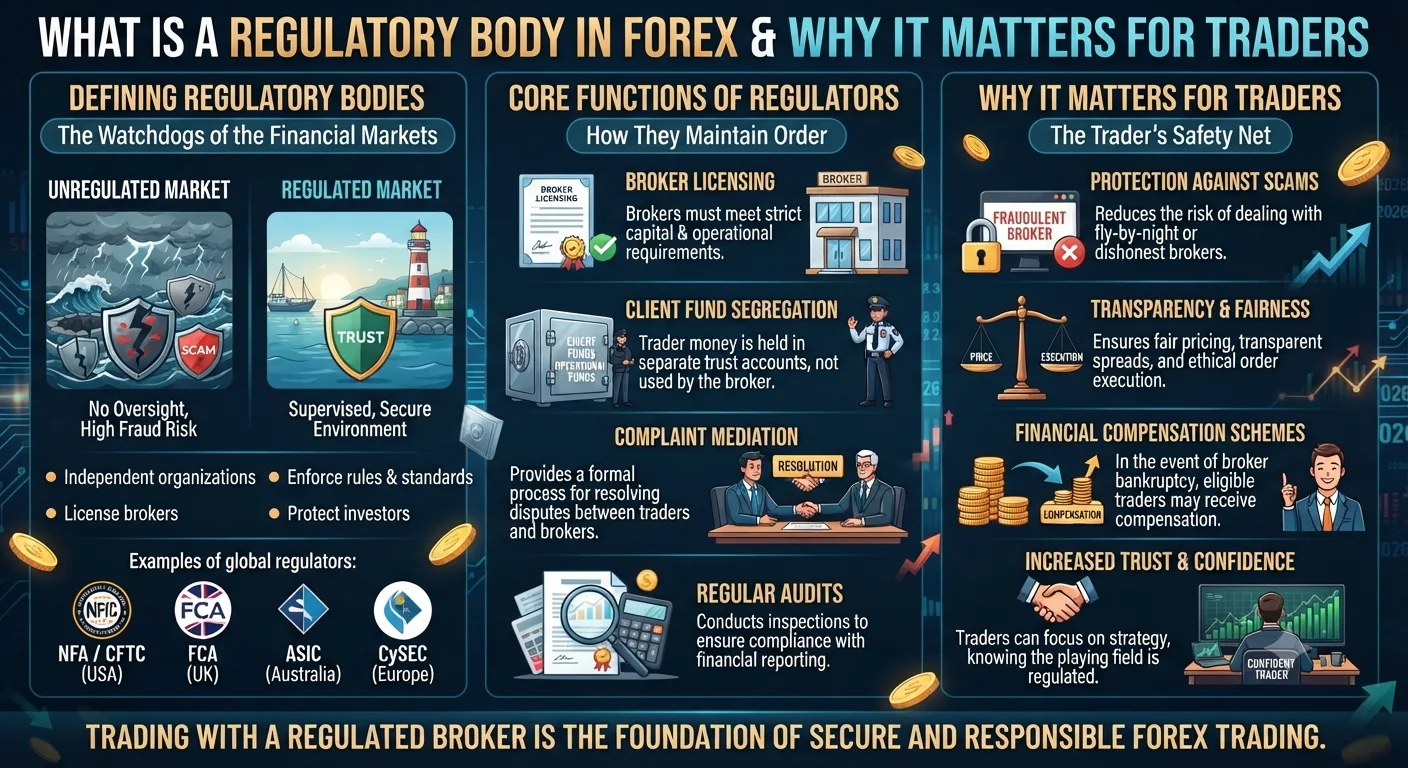

A regulatory body in forex is a government-appointed or government-recognised authority that licenses, monitors and enforces rules for companies offering forex trading services to retail clients. Regulatory bodies exist to protect traders from fraud, unfair practices and broker insolvency. Choosing a broker regulated by a credible authority is the single most important safety step any forex trader can take.

Quick Definition: What Is a Regulatory Body?

In everyday life regulatory bodies set and enforce the rules businesses must follow in their industry. A food safety authority regulates restaurants. A financial regulatory body does the same for financial services companies including forex brokers.

When a forex broker is regulated by a recognised authority it means:

- The broker has applied for and been granted a licence after meeting specific capital, operational and conduct requirements

- The broker is subject to ongoing supervision including financial reporting, conduct monitoring and regular audits

- Retail clients have access to a formal complaints and dispute resolution process

- In many jurisdictions clients are protected by a compensation scheme if the broker fails

Without regulation none of these protections exist. The broker can operate however it chooses and a trader whose funds are lost to an unregulated broker has no legal recourse.

How It Works in Real Forex Trading

- Quick Definition: What Is a Regulatory Body?

- How It Works in Real Forex Trading

- The Major Forex Regulatory Bodies

- Regulatory Tiers: Not All Regulators Are Equal

- A Practical Example

- Frequently Asked Questions

- Q: How do I check if a forex broker is genuinely regulated?

- Q: What is the difference between FCA and CySEC regulation?

- Q: Can a broker be regulated in one country and still scam clients?

- Q: Why do some brokers hold multiple regulatory licences?

When a regulated broker accepts a client deposit the regulatory framework determines what happens to those funds, how trades must be executed and what the broker must disclose. Here is how the framework operates in practice:

Licensing: The broker applies to the regulatory body, provides proof of sufficient capital, demonstrates adequate systems and controls and passes background checks on its directors and owners. Only brokers that meet these requirements receive a licence.

Ongoing supervision: Once licensed the broker submits regular financial reports to the regulator, undergoes periodic audits and must report significant events such as large client losses or operational failures.

Client fund protection: Licensed brokers in most major regulatory frameworks must hold retail client funds in segregated bank accounts separate from the broker's own money. This ring-fences client funds from the broker's creditors in the event of insolvency.

Conduct rules: Brokers must provide fair and accurate pricing, execute client orders on a best-execution basis, disclose all fees clearly and avoid misleading marketing. Violations can result in fines, licence suspension or criminal prosecution.

Complaints process: Regulated brokers must have a formal internal complaints procedure. In many jurisdictions clients who are not satisfied with the broker's response can escalate to an independent ombudsman or the regulator itself.

The Major Forex Regulatory Bodies

| Regulatory Body | Jurisdiction | Known For |

|---|---|---|

| Financial Conduct Authority (FCA) | United Kingdom | One of the most rigorous retail trader protection frameworks globally |

| Australian Securities and Investments Commission (ASIC) | Australia | Strong conduct rules and reduced leverage limits introduced in 2021 |

| Cyprus Securities and Exchange Commission (CySEC) | Cyprus / EU | Primary regulator for many EU-passported forex brokers |

| Commodity Futures Trading Commission (CFTC) | United States | Strict rules, limited broker choice for US residents |

| Monetary Authority of Singapore (MAS) | Singapore | Highly respected regulator in the Asia-Pacific region |

| Financial Sector Conduct Authority (FSCA) | South Africa | Growing enforcement capability in a large African retail market |

| Dubai Financial Services Authority (DFSA) | UAE / DIFC | Covers brokers operating within the Dubai International Financial Centre |

Regulatory Tiers: Not All Regulators Are Equal

A critical point that many beginner traders miss is that a regulated broker is not automatically safe. The quality of the regulatory framework matters enormously.

Recommended Articles

FOREX REGULATIONS LEGAL GUIDES

FOREX REGULATIONS LEGAL GUIDES

Tier 1 regulators such as the FCA and ASIC have strict capital requirements, active enforcement records, mandatory client fund segregation and compensation schemes. A licence from these bodies provides meaningful protection.

Tier 2 regulators such as CySEC provide reasonable but somewhat less stringent oversight. Most CySEC brokers operating under EU passporting rules must comply with ESMA requirements which strengthens the framework significantly.

Offshore regulators in jurisdictions such as Vanuatu, the Marshall Islands, Saint Vincent and the Grenadines or Seychelles often issue licences with minimal requirements and very little ongoing oversight. A broker claiming to be regulated by one of these bodies provides almost no meaningful protection to retail traders.

Always check which specific regulatory body a broker holds a licence with before depositing funds.

A Practical Example

A trader in Pakistan searches for a forex broker and finds one displaying both an FCA logo and a Vanuatu Financial Services Commission (VFSC) logo on its homepage.

The trader visits the FCA's Financial Services Register and searches for the broker's name. The search returns no results or returns the broker as having a different status such as an appointed representative rather than a directly authorised firm.

The trader then checks the Vanuatu FSC register and finds the broker listed but notes that Vanuatu does not require segregated client accounts or maintain a compensation scheme.

This broker is effectively unregulated for the level of protection that matters. The prudent action is to choose a broker with a verifiable active licence from the FCA, ASIC or another Tier 1 regulator and to confirm the licence status directly on that regulator's public register.

Frequently Asked Questions

Q: How do I check if a forex broker is genuinely regulated?

Go directly to the regulatory body's official website and search their public register using the broker's name or licence number. Do not rely on regulatory logos displayed on the broker's website. The FCA register is at register.fca.org.uk. The ASIC register is at search.asic.gov.au. CySEC's register is at cysec.gov.cy. Always verify directly.

Q: What is the difference between FCA and CySEC regulation?

Both are legitimate regulators operating under EU-origin frameworks. The FCA regulates brokers in the United Kingdom and is generally considered to operate a stricter and more actively enforced framework. CySEC regulates brokers in Cyprus and EU member states. CySEC brokers that are fully MiFID-compliant benefit from ESMA-level consumer protections including negative balance protection and leverage limits. The primary practical difference is the compensation scheme: the UK FSCS covers up to GBP 85,000 while the Cyprus Investor Compensation Fund covers up to EUR 20,000.

Q: Can a broker be regulated in one country and still scam clients?

Regulatory oversight reduces the risk of fraud but does not eliminate it entirely. Even regulated brokers have been subject to enforcement action for misconduct. Regulation provides a framework of protection and recourse, not an absolute guarantee. This is why choosing a broker with a strong regulatory track record from a Tier 1 regulator and reading independent reviews matters in addition to simply confirming a licence exists.

Q: Why do some brokers hold multiple regulatory licences?

Large international brokers often hold licences in multiple jurisdictions to legally serve clients from different countries. A broker may hold an FCA licence to serve UK clients, a CySEC licence to serve EU clients and an ASIC licence to serve Australian clients with each licence requiring compliance with that jurisdiction's specific rules. Multiple licences from credible regulators generally indicate a well-established, compliant operation.