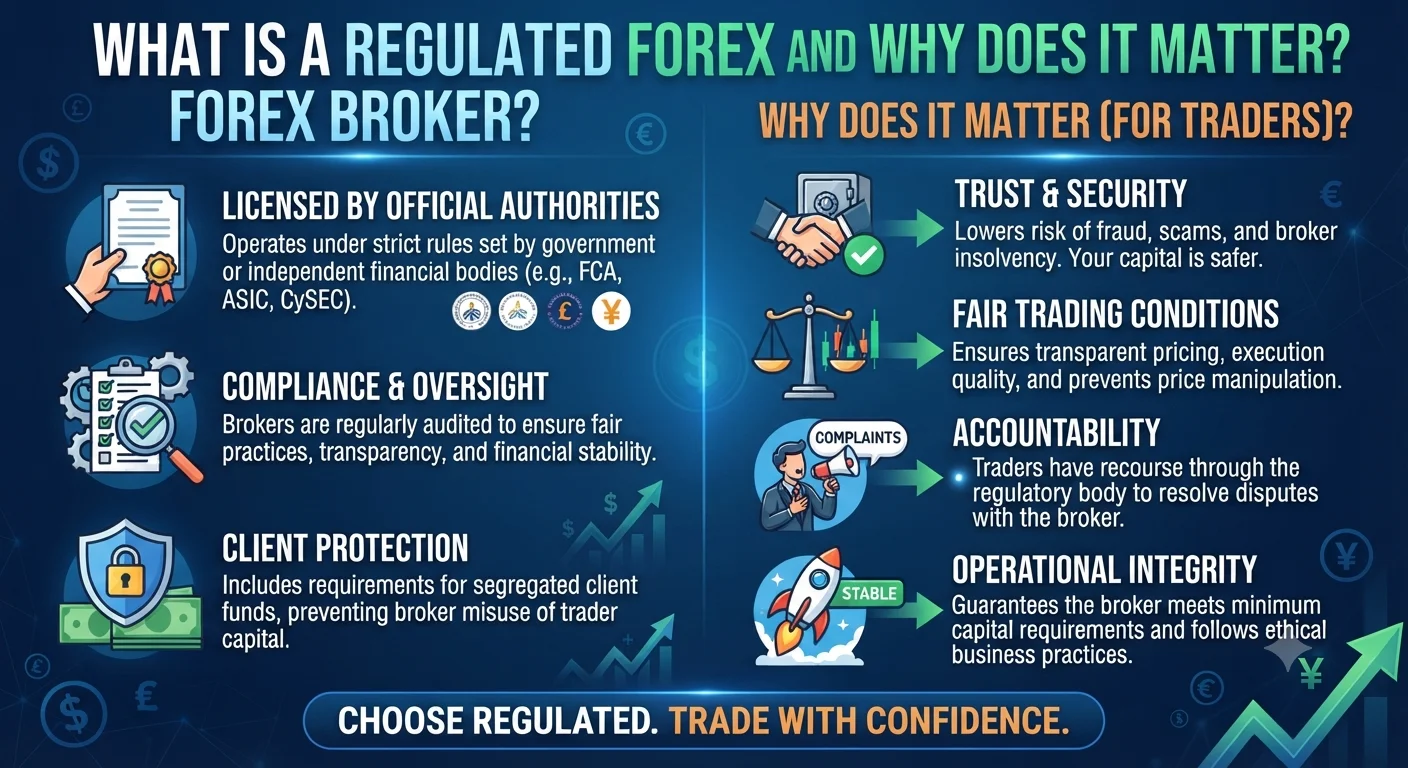

A regulated forex broker is a company that has been licensed by a recognised government financial authority to offer forex trading services to retail clients. Regulation means the broker must follow legally binding rules about how client funds are held, how trades are executed and how complaints are handled. Without regulation there is no legal framework protecting your money if something goes wrong.

Quick Definition: What Is a Regulated Forex Broker?

When a forex broker applies for regulation in a jurisdiction they submit to an oversight framework that typically requires them to:

- Hold client funds in segregated accounts separate from the broker's own operating funds

- Maintain a minimum level of capital reserves to cover client obligations

- Follow fair execution rules that prevent deliberately poor trade fills

- Provide regular financial reporting to the regulator

- Offer a process for client complaints and dispute resolution

- In many jurisdictions contribute to an investor compensation scheme

These requirements exist because retail forex traders are considered vulnerable participants in a complex financial market. Regulation creates a layer of structural protection that an unregulated broker simply does not offer.

How It Works in Real Forex Trading

- Quick Definition: What Is a Regulated Forex Broker?

- How It Works in Real Forex Trading

- A Practical Example

- Why It Matters for Your Trading Results

- Frequently Asked Questions

- Q: How do I verify if a forex broker is regulated?

- Q: Is an offshore regulated broker as safe as an FCA or ASIC broker?

- Q: What is negative balance protection?

- Q: What is a segregated client account?

- Q: Can a broker be regulated in one country and still accept clients from another?

The practical difference between trading with a regulated versus an unregulated broker shows up most clearly when something goes wrong.

Scenario 1: Regulated broker

A trader deposits $5,000 with an FCA-regulated broker. The broker keeps those funds in a segregated client account at a major bank. If the broker becomes insolvent the client funds are ring-fenced and cannot be used to pay the broker's creditors. Under the UK Financial Services Compensation Scheme eligible clients may recover up to $85,000 if the segregated funds are insufficient. The trader files a complaint and has access to the Financial Ombudsman Service.

Scenario 2: Unregulated broker

A trader deposits $5,000 with an offshore unregulated broker. There is no requirement for the broker to segregate client funds. If the broker becomes insolvent or simply stops operating the trader has no legal recourse. There is no regulatory body to complain to and no compensation scheme. The $5,000 is gone.

This is not a hypothetical scenario. Retail forex traders lose significant funds to unregulated or fraudulent brokers every year.

A Practical Example

A trader in the UK opens an account with a broker that displays an FCA logo on its website. Before depositing they go to the FCA's official Financial Services Register at register.fca.org.uk and search for the broker's name.

The search confirms the broker holds a valid FCA licence with an active status and the firm's registered address and permitted activities are listed. The trader can see the broker is authorised to deal in investments and arrange transactions as a retail broker.

Recommended Articles

BROKER PLATFORM REVIEWS

BROKER PLATFORM REVIEWS

This 60-second verification step is the single most important action any trader can take before depositing funds with any broker.

Why It Matters for Your Trading Results

Choosing a regulated broker does more than protect your funds. It also affects your day-to-day trading experience:

Execution quality: Regulated brokers are required to achieve best execution for client orders. This limits the ability to artificially widen spreads or delay fills to the broker's advantage.

Transparent pricing: Regulatory rules require brokers to clearly disclose their spreads, commissions and any other fees before a client opens an account.

Negative balance protection: In the EU, UK and Australia regulated brokers are required by law to offer retail clients negative balance protection, meaning your account cannot go below zero regardless of market conditions.

Leverage limits: Regulated brokers must apply the leverage limits set by their regulator for retail clients. While some traders see this as a restriction it also limits the risk of catastrophic losses from over-leveraging.

Frequently Asked Questions

Q: How do I verify if a forex broker is regulated?

Go directly to the regulatory authority's official website and use their public register to search for the broker by name or licence number. Do not trust a regulatory logo displayed on the broker's website without independently verifying it. The major registers include the FCA Register for UK brokers, ASIC Connect for Australian brokers and the CySEC register for EU brokers.

Q: Is an offshore regulated broker as safe as an FCA or ASIC broker?

Not necessarily. Some offshore jurisdictions offer very little meaningful oversight despite issuing licences. Regulation from the FCA, ASIC, CySEC, MAS or CFTC provides significantly stronger legal protections than regulation from many smaller offshore jurisdictions. The quality of the regulatory framework matters as much as the existence of a licence.

Q: What is negative balance protection?

Negative balance protection is a guarantee from the broker that your account balance cannot fall below zero. In highly volatile market conditions leverage can theoretically cause losses exceeding your deposit. Negative balance protection means the broker absorbs any such excess loss rather than billing you for it. It is mandatory for retail clients under FCA, ESMA and ASIC rules.

Q: What is a segregated client account?

A segregated client account is a bank account where client funds are held completely separately from the broker's own operational funds. If the broker goes bankrupt its creditors cannot access the segregated client funds. This is a fundamental requirement of all reputable regulatory frameworks and the most direct protection for trader deposits.

Q: Can a broker be regulated in one country and still accept clients from another?

Yes. Many brokers hold a single regulation from one jurisdiction but accept clients globally. In most cases this is legal for the client. However it means the client may have less protection than they would if the broker held a local licence. Some regulators such as the FCA have restrictions on overseas promotion that limit which brokers can actively market to UK residents.